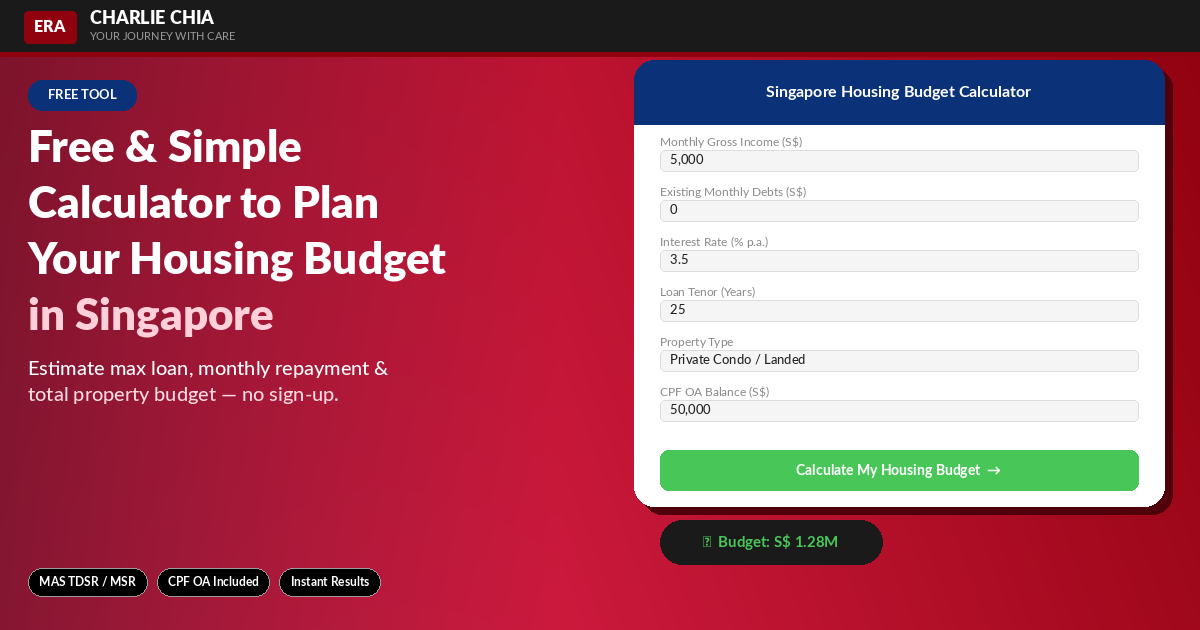

Buying a property in Singapore (whether your first HDB flat, a resale unit, or a condominium) starts with one critical question: how much can I actually afford? Use the free mortgage calculator and loan calculator below which will help you estimate your maximum loan, monthly repayments, and total housing budget in minutes (no sign-up required).

How Borrowing Limits Work in Singapore

Before using the calculator, two key frameworks govern how much you can borrow:

Total Debt Servicing Ratio (TDSR)

TDSR caps your total monthly debt obligations — home loan, car loan, credit cards, and all other loans — at 55% of your gross monthly income. This applies to all property types.

Mortgage Servicing Ratio (MSR)

MSR applies specifically to HDB flats and Executive Condominiums (ECs). It limits your monthly HDB or EC loan repayment to 30% of your gross monthly income. If you are buying a private condominium, only TDSR applies.

⚠ Please fill in all required fields with valid values.

Based on your income and debt obligations, there is no remaining capacity for a home loan under MAS guidelines. Consider clearing existing debts before applying.

- Cash (Min. Down Payment) 5% —

- CPF OA / Cash 20% —

- Bank Loan Amount 75% —

* Estimates are based on MAS TDSR/MSR guidelines and a 75% LTV ratio (first loan, no outstanding home loans). The minimum cash down payment is 5% of purchase price; a further 20% can be paid using CPF OA. Actual approval depends on credit assessment, age, and lender policies. Speak to a licensed mortgage advisor for a full assessment.

Tips to Maximise Your Housing Budget

- Clear existing debts first — Reducing car loan or credit card balances directly increases your TDSR headroom

- Top up your CPF OA — Voluntary top-ups can boost your Ordinary Account balance, reducing cash required for downpayment

- Choose your loan tenor carefully — A longer tenor reduces monthly repayments but increases total interest paid

- Factor in all purchase costs — Buyer’s Stamp Duty (BSD), Additional Buyer’s Stamp Duty (ABSD if applicable), legal fees, and renovation costs can add 5–10% to your total outlay

- Get an In-Principle Approval (IPA) — Secure your bank IPA before making any offers so you know exactly what you are working with

HDB Loan vs Bank Loan: Which Is Better?

| Factor | HDB Loan | Bank Loan |

|---|---|---|

| Interest Rate | 2.6% (CPF-OA rate + 0.1%) | From ~2.5–3.8% (variable) |

| LTV Limit | Up to 75% | Up to 75% |

| Downpayment | 25% (all CPF allowed) | 25% (minimum 5% in cash) |

| Eligibility | HDB flats only; income ceiling applies | All property types |

| Flexibility | Fixed rate; no refinancing | Refinancing options available |

Note: Data is accurate as of 6 April 2026 and may be subject to change.

Need Help Planning Your Property Budget?

Numbers on a calculator are just a starting point. A trusted real estate agent in Singapore can review your CPF usage, stamp duty obligations, renovation budget, and long-term financial goals to make sure every dollar is working as hard as possible for your family.

Speak to Charlie Chia for a free, no-pressure property budget consultation. No obligations — just honest, clear guidance.

FAQs

What is the TDSR limit in Singapore?

The Total Debt Servicing Ratio (TDSR) limit is 55% of your gross monthly income. All existing monthly debt obligations count towards this limit.

What is the MSR limit for HDB flats?

The Mortgage Servicing Ratio (MSR) limits HDB and EC loan repayments to 30% of your gross monthly income.

How much cash do I need to buy a condo in Singapore?

For a bank loan on a private property, you need at least 5% of the purchase price in cash as part of the 25% downpayment. The remaining 20% can be paid via CPF.

Can I use my CPF to pay for a private condominium?

Yes. CPF Ordinary Account savings may be used for downpayment and monthly repayments on private property, subject to the property’s remaining lease and applicable CPF usage limits.